SMM February 13 News:

The monthly charts of the world's three major copper futures showed gains in January, driven by concerns over intensified global trade conflicts triggered by US President Trump's tariffs. COMEX copper futures led with a monthly increase of 6.12%, significantly outpacing SHFE copper and LME copper, which rose 2.36% and 3.42%, respectively. Entering February, external macro sentiment repeatedly disrupted the market, and the US dollar index overall pulled back. The tight copper ore supply persisted, with the SMM Imported Copper Concentrate Index (weekly) falling into negative territory for two consecutive weeks. As the Two Sessions approach, market expectations for favourable macro policies in China have risen, further boosting copper prices. As of 15:20 on February 13, the COMEX copper monthly chart for February temporarily rose 10.43%, LME copper rose 4.35%, and SHFE copper rose 2.66%.

》Click to view the SMM Futures Data Dashboard

Fundamentals

The Copper Concentrate Index Continued to Weaken in January; Imported Copper Concentrate Index (weekly) Fell into Negative Territory for Two Consecutive Weeks

》Click to view SMM Spot Copper Prices

》Subscribe to view historical price trends of SMM Metal Spot Prices

According to SMM quotes, the SMM Copper Concentrate Index (monthly) for January 2025 was $1.76/mt, down $6.33/mt from December 2024. Reviewing its historical price trends, the SMM Copper Concentrate Index (monthly) peaked at $10.38/mt in November 2024 before pulling back in December 2024 and January 2025. Notably, as the copper ore market remained tight in January, the Copper Concentrate Index continued to weaken. Furthermore, the SMM Imported Copper Concentrate Index (weekly) fell into negative territory for two consecutive weeks, with the February 7 reading at -$2.70/mt, down $0.5/mt from the previous week's -$2.20/mt.

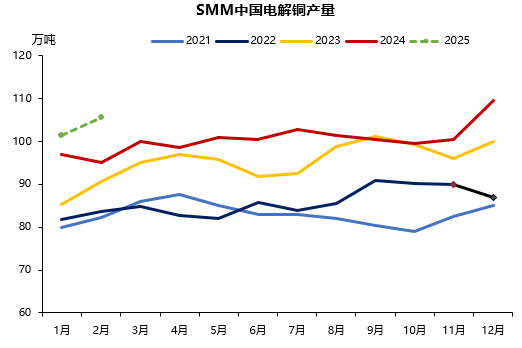

January Copper Cathode Production Fell 7.46% MoM; February Production Is Expected to Increase MoM

》Click to view the SMM Metal Industry Chain Database

Domestic Production: In January, SMM China's copper cathode production decreased by 81,700 mt MoM, a decline of 7.46%, but increased by 4.54% YoY, exceeding expectations by 6,500 mt. The significant decline in January production was mainly due to the following reasons: 1. Some smelters had a shortened statistical period from January 1 to January 25, leading to a noticeable drop in production; 2. Two smelters underwent maintenance in January, contributing to the decline; 3. Many smelters experienced varying degrees of production decline due to tight copper concentrate and blister copper supply (as of January 24, the SMM Copper Concentrate Index (monthly) was $1.76/mt, and the SMM Domestic Blister Copper RC (weekly) was 800 yuan/mt).

Based on production schedules, SMM expects domestic copper cathode production in February to increase by 41,600 mt MoM, a rise of 4.1%, and by 105,100 mt YoY, a rise of 11.06%. 》Click to view details

Copper Semis Industry Operating Rates Declined in January; Limited Growth Expected in February

Regarding copper semis operating rates, the copper semis industry experienced a seasonal decline in January due to the Chinese New Year holiday and the completion of export rush orders. As some enterprises will not fully resume operations until after the Lantern Festival (February 12), the overall increase in copper semis operating rates in February is expected to be limited.

Copper Rods: According to SMM, the operating rates of copper cathode rod enterprises declined MoM in January. On a lunar calendar basis, due to differences in the Chinese New Year period, operating rates increased YoY. As the holiday approached, copper prices rebounded in January. SMM data showed that the average price of SMM #1 copper cathode in January was 75,023.61 yuan/mt, up 581.56 yuan/mt MoM. The price spread between copper cathode rods and secondary copper rods widened. According to SMM statistics, the average price spread between secondary copper rods in Jiangxi and power rods in east China was 1,218 yuan/mt in January, up 412 yuan/mt MoM, reducing the advantage of copper cathode rods. Additionally, as copper prices rose and news of US tariff increases emerged, some downstream enterprises were concerned about a potential pullback in copper prices during and after the holiday. Pre-holiday restocking consumption was not significant, as substantial consumption had already been released during the year-end push for annual targets when copper prices were low. Consequently, as the holiday atmosphere intensified in January, some copper cathode rod enterprises entered the holiday period early. In the first half of February, the holiday atmosphere persisted, with many downstream enterprises yet to resume operations. Meanwhile, post-holiday copper prices continued to rise strongly, and downstream restocking activity remained subdued, with weak new orders. 》Click to view details

Copper Pipes: According to SMM data, the operating rates of copper pipe enterprises declined both MoM and YoY in January. As the Chinese New Year holiday approached, operating rates diverged significantly among large, medium, and small enterprises. Large copper pipe enterprises generally did not shut down during the holiday, flexibly adjusting production based on orders. Although some production lines were reduced, sufficient orders from air conditioner manufacturers and export orders provided support, leading to improved overall order conditions compared to last year. Medium-sized copper pipe enterprises had holiday durations ranging from 0 to 6 days, resulting in uneven operating rates. Enterprises with support from export orders and large manufacturers' orders achieved operating rates close to 70%, but weak orders in the installation pipe market dragged down overall performance. Small copper pipe enterprises had operating rates of only 56.39%, with weak orders in the hardware and sanitary ware market at the beginning of the year, while military orders remained stable. Although some brass pipes were supported by export orders, their small base limited their contribution to operating rates. 》Click to view details

Wire and Cable: According to SMM, the operating rates of copper wire and cable enterprises declined both MoM and YoY in January. The main reasons for the decline included the Chinese New Year holiday, which led most enterprises to shut down, with some retaining minimal production lines; rising copper prices in January, which dampened customer purchasing enthusiasm; and gradually weakening demand after a moderately strong market in early January. Notably, demand for medium- and low-voltage orders for construction and infrastructure weakened significantly, while power generation orders also softened. Only power grid orders remained relatively stable. Some enterprises accelerated production in late December 2024 to meet year-end targets, which preemptively consumed January production. Post-holiday, production recovery was slow, with enterprises primarily consuming finished product inventories. 》Click to view details

Inventory: Copper Inventories in Major Domestic Regions Rose to 326,200 mt; LME Copper Inventories Showed Destocking Recently

SMM Copper Inventories in Major Domestic Regions: Copper inventories in major domestic regions tracked by SMM began to rise from 103,000 mt on Monday, January 13. As of Thursday, February 13, inventories increased by 21,400 mt from Monday to 326,200 mt, up 53,100 mt WoW and 160,400 mt from pre-Chinese New Year levels. The post-holiday inventory buildup exceeded last year's by 42,300 mt in the first week. Specifically, Shanghai inventories rose by 13,900 mt from Monday to 189,400 mt, driven by arrivals of both domestic and imported copper. Notably, a significant amount of domestic copper was delivered to warehouses for settlement. Currently, Shanghai warehouse warrants stand at 41,800 mt, up 29,300 mt from pre-holiday levels, contributing significantly to the inventory increase. Jiangsu inventories rose by 4,700 mt to 58,600 mt, while Guangdong inventories rose by 4,000 mt to 66,900 mt. Inventory buildup in these two regions was relatively small due to the gradual recovery of downstream consumption.

Looking ahead, as delivery approaches, SMM expects domestic copper deliveries to warehouses to increase, with imported copper also arriving steadily. Total supply is expected to remain abundant. On the demand side, downstream enterprises are expected to fully resume production after the Lantern Festival, leading to increased demand. Therefore, SMM anticipates a scenario of rising supply and demand next week, with supply growth likely outpacing demand growth, resulting in continued weekly inventory increases. 》Click to view details

Overseas Copper Inventories: LME copper inventories stood at 271,400 mt on December 31, 2024, and decreased to 256,225 mt on January 31, 2025, showing a slight destocking trend in January. This trend continued into February, with LME copper inventories falling to 237,925 mt as of February 13. COMEX copper inventories were 93,161 short tons on December 31, 2024, and increased to 98,237 short tons on January 31, 2025. The widening price spread between COMEX and LME copper led to changes in international trade flows of copper cathode starting in January 2025: First, deliverable COMEX copper cathodes in LME Asian warehouses were continuously cancelled and shipped to North America; second, shipments from South America to Asia decreased, with some long-haul shipments delayed; third, some African shipments were sent to North America during the Chinese New Year holiday. These factors contributed to the continued rise in COMEX copper inventories, which reached 100,341 short tons on February 12.

Outlook

Looking ahead, on the macro front, US inflation exceeded expectations last month. The US Consumer Price Index (CPI) rose 0.5% in January, surpassing the expected 0.3% and marking the largest MoM increase since August 2023. The CPI rose 3% YoY, compared to economists' expectations of 2.9%. Core CPI rose 3.3% YoY, exceeding the expected 3.1%. Interest rate futures traders currently anticipate a 27-basis-point rate cut by year-end, implying a high likelihood of only one 25-basis-point rate cut for the year, compared to pre-data expectations of a 37-basis-point cut. The market will continue to assess the impact of US tariffs, with frequent adjustments to tariff policies maintaining significant uncertainty. Future attention will focus on tariff-related developments affecting the copper market. Additionally, January PMI data from China and the US will be noteworthy. As the Two Sessions approach, attention will also be given to relevant macro information and statements from representatives.

On the fundamentals side, the tight copper ore supply continues to support copper prices. Domestic copper inventories have risen above 320,000 mt, and downstream consumption remains in the off-season. High copper prices are suppressing downstream restocking sentiment. Overseas, LME copper inventory destocking will support LME copper prices. COMEX copper inventories have risen above 100,000 short tons. Once market concerns over Trump's tariffs ease, COMEX copper inventories are expected to weigh on COMEX copper market performance.

In summary, as the Two Sessions approach, domestic market expectations for favourable macro policies may support copper prices. However, concerns over global trade conflicts triggered by US tariff policies may repeatedly affect market sentiment, thereby disrupting copper prices. On the fundamentals side, copper prices will be supported by tight raw material supply. However, downstream copper consumption remains in the off-season, and high copper prices are suppressing downstream consumption sentiment, weakening support from the demand side. Combined with domestic copper inventory buildup, these factors will limit the upside for domestic copper prices, as reflected in the monthly gains of the three major futures exchanges. Nevertheless, after the record-high premium of COMEX copper over LME copper, the recent pullback in COMEX copper prices still leaves a price spread of several hundred dollars, which may influence SHFE copper. Future attention should focus on the macro impact on copper price trends and whether market sentiment regarding tight copper ore supply will continue to intensify as the Copper Concentrate Index falls into negative territory.

Institutional Comments

A research report by Guosen Futures pointed out that on Thursday, SHFE copper rose, with the most-traded contract increasing by over 8,000 lots. In the spot market, copper prices increased, but market transactions were limited. Macro-wise, concerns about future inflation rebound, further escalation of trade frictions, and declining demand are expected to amplify the volatility of metal prices. Fundamentally, China's copper consumer market is gradually recovering, but downstream demand overall remains in the off-season recovery phase. Inventory buildup during the holiday period is also expected to weigh on copper prices. According to SMM data, as of Thursday, February 13, copper inventories in major regions nationwide increased by 21,400 mt from Monday to 326,200 mt, up by 53,100 mt from last Thursday and by 160,400 mt compared to pre-Chinese New Year levels. The post-holiday first-week inventory buildup exceeded the same period last year by 42,300 mt. Overall, fundamentals provide limited upward momentum for copper prices. Attention should be paid to changes in macro sentiment affecting copper prices. SHFE copper, approaching recent highs, faces certain resistance above, and is expected to fluctuate, with a range-bound trading strategy recommended.

A research report by China Fortune Futures stated: Copper has shown renewed strength, approaching previous highs. As February enters its latter half, the market will gradually focus on policy expectations for the Two Sessions in March. A relatively positive trading strategy is maintained, with further rebounds in copper and aluminum expected to reach higher levels.

Goldman Sachs stated that their baseline forecast includes a 70% probability of the US imposing a 10% tariff on copper imports by the end of 2025.

The Chilean Copper Commission projected that the average copper price will be $4.25/lb in 2025 and $4.25/lb in 2026.

Citi believes that further tariff escalation will lead to a bullish outlook for gold within 6-12 months, with gold prices rising to $3,000/oz. They are also bullish on silver, expecting it to rise to $36/oz, while maintaining a bearish outlook on copper prices, predicting a decline to $8,500/mt within the next three months.

Recommended Reading:

》Copper Inventories in Major Regions Nationwide Increased by 21,400 mt This Week [SMM Weekly Data]

For more information on copper market fundamentals, prices, and policy and technical insights, please join the CCI2025SMM (20th) Copper Industry Conference and Copper Industry Expo~